The below mentioned article provides a note on the Disclosure and Consideration for Amalgamation.

Disclosures made for Amalgamations:

For all amalgamations, the following disclosures should be made in the first financial statements following the amalgamation:

(a) Names and general nature of business of the amalgamating companies;

(b) Effective date of amalgamation for accounting purposes;

ADVERTISEMENTS:

(c) The method of accounting used to reflect the amalgamation; and

(d) Particulars of the scheme sanctioned under a statute.

For amalgamations accounted for under the pooling of interests method, the following additional disclosures should be made in the first financial statements following the amalgamation:

(a) Description and number of shares issued, together with the percentage of each company’s equity shares exchanged to effect the amalgamation;

ADVERTISEMENTS:

(b) The amount of any difference between the consideration and the value of net identifiable assets acquired, and the treatment thereof including the period of amortisation of any goodwill arising on amalgamation.

For amalgamations accounted for under the purchase method, the following additional disclosures should be made in the first financial statements following the amalgamation:

(a) Consideration for the amalgamation and a description of the consideration paid or contingently payable; and

(b) The amount of any difference between the consideration and the value of net identifiable assets acquired, and the treatment thereof including the period of amortisation of any goodwill arising on amalgamation.

ADVERTISEMENTS:

Amalgamation after the balance sheet date: When an amalgamation is effected after the balance sheet date but before the issuance of the financial statements of either party to the amalgamation, disclosure should be made in accordance with AS 4 (Revised), ‘Contingencies and Events Occurring after the Balance Sheet Date’, but the amalgamation should not be incorporated in the financial statements.

In certain circumstances, the amalgamation may also provide additional information affecting the financial statements themselves, for instance, by allowing the going concern assumption to be maintained.

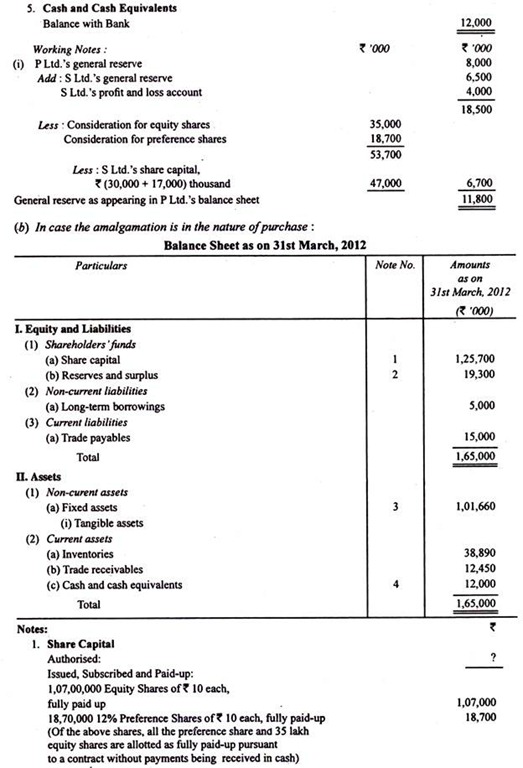

Now, study the following illustration carefully:

Illustration 1:

ADVERTISEMENTS:

The following information has been extracted from the balance sheets of P Ltd. and S Ltd. as on 31st March, 2012:

P Ltd. takes over S Ltd. on 1st April, 2012, and discharges consideration for the business as follows:

(i) Issued 35 lakh fully paid equity shares of Rs 10 each at par to the equity shareholders of S Ltd.

ADVERTISEMENTS:

(ii) Issued fully paid 12% preference shares of Rs 10 each to discharge the preference shareholders of S Ltd. at a premium of 10%.

It is agreed that the debentures of S Ltd. will be converted into equal number and amount of 10% debentures of P Ltd.

You are required to show the balance sheet of P Ltd. assuming that:

(a) The amalgamation is in the nature of merger, and

ADVERTISEMENTS:

(b) The amalgamation is in the nature of purchase.

[Adapted B.Com.(Hons.) Delhi – 2001]

Consideration Required for Amalgamation:

For the purpose of accounting for amalgamation, Accounting Standard 14 (AS-14) defines the term ‘consideration’ as “the aggregate of the shares and other securities issued and the payment made in the form of cash or other assets by the transferee company to the shareholders of the transferor company”.

Consideration implies the value agreed upon for the net assets taken over. The amount depends on the terms of the contract between the transferor company and the transferee company.

The consideration for amalgamation may consist of shares and other securities, cash and other assets and the amount of consideration depends upon the fair value of its elements. In case of issue of securities, the value fixed by the statutory authorities may be taken to be the fair value. In case of other assets, the fair value may be determined by reference to the market value of the assets given up.

Where the market value of the assets given up cannot be reliably assessed, such assets are valued at their respective net book values.

Where the scheme of amalgamation provides for an adjustment to the consideration contingent on one or more future events, the amount of the additional payment it included in the consideration if payment is probable and a reasonable estimate of the amount can be made. In all other cases, the adjustment is recognised as soon as the amount is determinable.

Where the scheme of amalgamation sanctioned under a statute prescribes the treatment to be given to the reserves of the transferor company after amalgamation, the same has to be followed.

ADVERTISEMENTS:

There are different methods in which consideration may be calculated:

i. Lump-sum Method:

It is the simplest method. In it, the consideration is stated as a lump-sum. For example, it may be stated that P Ltd. takes over the business of S Ltd for Rs 50,00,000. Here, the sum of Rs 50,00,000 is the consideration.

ii. Net Assets Method:

Under this method, the consideration is arrived at by adding the agreed values of all the assets taken over by the transferee company and deducting therefrom the agreed values of the liabilities taken over by the transferee company. The agreed value means the amount at which the transferor company has agreed to sell and the transferee company has agreed to take over a particular asset or a liability.

In the absence of any statement to the contrary regarding the agreed value of an asset or a liability, the amount at which the asset or the liability appears in the books of the transferor company is considered to be the agreed value.

Items of negative reserve and surplus (Preliminary Expenses, Underwriting Commission, Discount on Issue of Shares, Discount on Issue of Debentures, Expenses on Issue of Debentures, debit balance of Statement of Profits & Loss, etc.) are not taken over.

The following is the balance sheet of A Ltd:

One must remember:

(a) To add the values of the assets taken over by the transferee company. Goodwill is invariably taken over by the transferee company. Prepaid expenses should be added.

(b) Not to add the assets not taken over, {e.g., balance with Bank in the above example) and the fictitious assets or expenses not written off. All items which appear in the balance sheet as negative reserves and the debit balance of statement of Profit and Loss, if any, should never be added.

(c) Not to deduct the liabilities not taken over by the transferee company but to deduct the agreed value of the liabilities taken over.

(d) Not to deduct such balances as Capital Reserve, Capital Redemption Reserve, Securities Premium Account, General Reserve, Debenture Redemption Reserve, Credit balance of statement of Profit and Loss, etc.—in fact, any account which denotes undistributed profits.

All such items appear under the heading ‘Reserves and Surplus’. However, if any, reserve or fund or a portion of any reserve and fund denotes liability to third parties, the same must be included in liabilities. Workmen Compensation Fund is an example.

A company may credit regularly a certain amount to Workmen Compensation Fund so that it at any time a liability arises to pay compensation to a worker or workers, this fund may be used. At the time of the liquidation of the company, the credit balance of this fund will represent accumulated profit to be distributed among the equity shareholders.

However, if at the time of liquidation there is a liability to pay compensation to any worker, the liability will be recorded and the fund will be reduced to the extent of the liability; only the balance will be treated as accumulated profit. Insurance Reserve is another example. However, Employees Provident Fund or Staff Provident Fund denotes a liability towards the employees of the company.

(e) That the expression ‘all assets’ includes cash and the “the business” standing alone means assets including cash and all the liabilities to outsiders. Both the expressions exclude expenses or losses not written off.

iii. Net Payment Method:

Under this method, consideration is ascertained by adding up the cash paid, agreed value of assets given and the agreed values of the securities allotted by the transferee company to the transferor company in discharge of consideration. Suppose, P Ltd. for business taken over from S Ltd. agrees to pay 15,00,000 in cash and allot to S Ltd. 4,00,000 equity shares of Rs. 10 each fully paid at an agreed value of Rs 15 per share.

In this case, the consideration will be ascertained as follows:

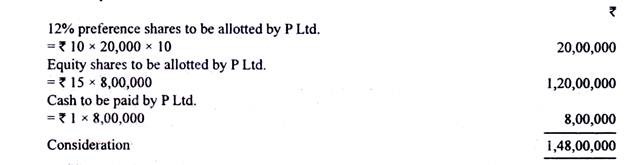

Suppose, P Ltd. takes over the business of S Ltd. and agrees to give for each J1% preference share in S Ltd. ten 12% preference shares of Rs 10 fully paid up at par and for each equity share in S Ltd. Re. 1 in cash and one fully paid equity share in P Ltd. of Rs 10 valued at Rs 15. The consideration will be computed as follows;

iv. Intrinsic Worth Method:

Consideration may have to be calculated on the basis of the agreed value of shares of the transferor company. Shares are ownership securities; if the transferee company pays for all the shares of the transferor company, it can be said to have paid for the entire business of the transferor company.

Suppose, the subscribed capital of S Ltd. consists of 6,00,000 equity shares of Rs 10 each fully paid and there are no preference shares.

Further suppose, P Ltd. takes over the business of S. Ltd and it is agreed between S Ltd. and P. Ltd. that the value of one share of S Ltd. is Rs 13; then the consideration will be Rs 13 x 6,00,000 = Rs 78,00,000. If the transferee company is to discharge the consideration in the form of its own equity shares, the agreed value of a share of transferee company also becomes relevant.

The consideration, divided by the agreed value of one share of Transferee Company will give the number of shares to be allotted by the transferee company to transferor company to discharge consideration.

In the abovementioned case, if P Ltd. is to discharge the consideration in the form of its own shares and if it is agreed between P Ltd. and S Ltd. that the value of one share of P Ltd. of the paid up value of Rs 10 is Rs 25, P Ltd. will allot 78,00,000/25=3,12,000 shares to S Ltd. to discharge the consideration.

At the time of allotment, P Ltd will debit liquidator in S Ltd. with Rs 78,00,000 (amount of consideration) and credit Equity Share Capital with Rs 31,20,000 (paid up value of the shares allotted) and Securities Premium Account with Rs 46,80,000 (the amount of securities premium charged @ Rs 15 per share).

The transferor company will debit Shares in Transferee Company Account and credit transferee company with the agreed value of shares received from transferee company.