In this article we will discuss about Current Cost Accounting (CCA):- 1. Definition of Current Cost Accounting (CCA) 2. Objectives of CCA 3. Evaluation.

Definition of Current Cost Accounting (CCA):

Current cost accounting uses “value to the business” as the measurement basis. Value to the business is defined as:

(a) Net current replacement cost or, if a permanent diminution to below net current replacement cost has been recognised;

(b) Recoverable amount. Recoverable amount is the greater of net realisable value of an asset and, where applicable, the amount recoverable from its further use.

ADVERTISEMENTS:

The ‘value to the business’ concept is illustrated in the following figure:

Where an asset will normally be replaced it is shown at the net current replacement cost, and charged on this basis in the profit and loss account. However, where it is not to be replaced or where replacement cost is higher than both net realisable value and present value, the higher of net realisable value and present value is usually used as the measurement basis.

The replacement cost of a specific asset is normally derived from the current acquisition cost of a similar asset, new or used, or of an equivalent productive capacity or service potential. Net realisable value usually represents the net current selling price of the asset. Present value represents a current estimate of future net receipts attributable to the asset, appropriately discounted.

Objectives of CCA:

Current Cost Accounting (CCA) aims to maintain capital of a business enterprise in terms of its operating capability. Operating capability is denoted by the net operating assets of the enterprise in terms of share-holders funds. As an equation,

ADVERTISEMENTS:

Net Operating assets = Total tangible assets + Net monetary working capital (current assets – current liabilities)

A change in the input prices of goods and services used and financed by the business will affect the amount of funds required to maintain the operating capability of the business enterprise. Therefore, maintaining the operating capability is the objective which is attempted to be achieved under CCA while preparing profit and loss account and balance sheet. CCA is based on UK accounting standard, SSAP 16 Current Cost Accounting, issued in 1980.

CCA aims to prepare the following:

ADVERTISEMENTS:

(A) Current Cost Profit and Loss Account (to determine Current Cost Operating profit).

(B) Current Cost Balance Sheet.

(A) Current Cost Profit and Loss Account:

In CCA, the profit and loss account is prepared to determine the current cost operating profit (CCOP). CCOP is determined after allowing for the impact of price changes, on the funds needed to continue the existing business and maintain its operating capability whether financed by share capital or borrowing. CCOP is calculated before interest on net borrowings and taxation.

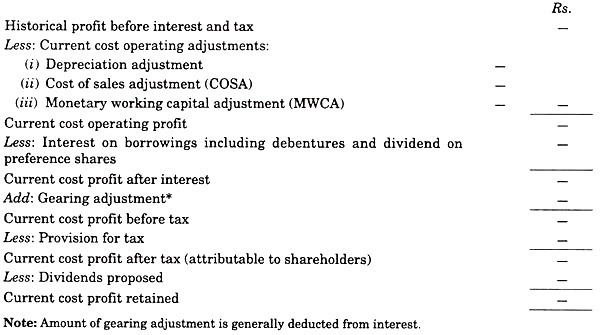

CCOP is determined after making the following three adjustments to historical cost profit before interest and taxes:

ADVERTISEMENTS:

(1) Depreciation Adjustment.

(2) Cost of Sales Adjustment (COSA).

(3) Monetary Working Capital Adjustment (MWCA).

After determining CCOP, interest and taxes are considered in current cost profit and loss account to finally ascertain net income under CCA. Net income under CCA can be defined as the surplus amount which can be distributed to proprietor or shareholders after keeping the operating capability of an enterprise intact.

ADVERTISEMENTS:

(1) Depreciation Adjustment:

This reflects the difference between depreciation calculated on the current cost of fixed assets and depreciation charged in computing the historical cost income. The accounting policy adopted for the purposes of calculating the historical cost profit should be followed when calculating the depreciation on the current cost of fixed assets.

The current cost depreciation charge may be calculated by revising the depreciation charge in accordance with change in the appropriate index level between the year of purchase of the asset and current year. This is illustrated by the following example.

A plant was purchased on January 1, 2005 for Rs. 1,20,000 when the price index was 100. The life of the plant was estimated to be 10 years having no scrap value. On December 31, 2009 the relevant price index was 150. The following calculations will be made to arrive at depreciation adjustment figure on December 31, 2009.

When fixed assets are revalued every year, there will also be a shortfall of depreciation representing the effect of price rise during the current year on the accumulated depreciation till date. This shortfall is called backlog depreciation which is the amount needed to cover total depreciation provision based on current cost at the year end.

This backlog depreciation arising out of increase in current costs could be charged either to the general reserves or against the related revaluation surplus on fixed assets. The former will ensure that the enterprise maintains its operating capital at the time of replacement of fixed assets. The latter procedure has been recommended in the UK Standard (SSAP 16).

(2) Cost of the Sales Adjustment (COSA):

The cost of the sales adjustment refers to the difference between current cost of inventories at the date of sale and amount charged as the cost of goods sold in computing the historical cost profit. Theoretically, current cost of sales should be determined on an item by item basis. In a real world situation, however, it would be impracticable to do so and therefore, groups of similar items may be used.

ADVERTISEMENTS:

The following example illustrates cost of sales adjustment. The following data relate to a company:

(3) Monetary Working Capital Adjustment (MWCA):

The MWCA reflects the amount of additional (or reduced) finance needed for monetary working capital as a result of changes in the input prices of goods and services used and financed by the business.

Monetary working capital (usually represented by the difference between trade debtors and trade creditors) is an integral part of the net operating asset of the business. In times of rising prices, a business needs more funds to finance monetary working capital. The adjustment reflects this additional need for funds.

ADVERTISEMENTS:

MWCA is calculated if debtors are more than the creditors. If creditors are more than the debtors, this is a minus net working capital. The minus excess (creditors-debtors) is not regarded as funding working capital and excluded. It is included in net borrowing for the purpose of calculating gearing ratio and gearing adjustment.

The MWCA is made in the calculation of current cost operating profit and takes the form of a charge or credit to profit and loss account with the corresponding credit or charge to the current cost reserve. SSAP 16 of UK requires that MWCA should include items used in day-to-day operating activities of the business.

It includes trade debtors (including trade bills receivables, prepayments) and trade creditors (including trade bills payable, accruals, expense creditors). MWCA should not include creditors or debtors relating to fixed assets bought or sold or under construction.

Calculating MWCA:

(i) Determine the items to be included in MWCA.

(ii) Determine separately the relevant indices to be used in adjusting debtors and creditors:

(a) The index for debtors should reflect changes in the current cost of goods and services sold attributable to change in input prices over the period the debt is outstanding. Indices of selling prices may be used where these provide a fair approximation of cost changes in amount and time.

(b) The index for creditors should reflect similar changes in the cost of items which have been financed by those creditors over the period the credit is outstanding.

(c) Where the percentage changes in the indices to be used on debtors and creditors are similar, a single index can be used and the adjustment can be determined in one calculation.

(iii) Apply relevant index or indices to debtors and creditors to determine MWCA. In principle, in calculating the adjustment on debtors the profit element in debtors should be excluded. However, the total amount of debtors can be used where this gives a fair approximation.

(iv) An averaging method, compatible with the method used for COSA, may be used to calculate the adjustment.

The following example illustrates the calculation of monetary working capital adjustment:

Net Monetary Working Capital in terms of current cost (Jan. 1) 20,000 X 110/100 = Rs. 22,000

(Dec. 31) 30,000 x 1107120 = Rs. 27,500

Change due to volume = Rs. 27,500 – Rs. 22,000 = Rs. 5,500

Total change = Rs. 30,000 – Rs. 20,000 = Rs. 10,000

Monetary working capital adjustment = Rs. 10,000 – Rs. 5,500 = Rs. 4,500

The following journal entry is made to record monetary working capital adjustment:

Profit and Loss A/c Dr. 4,500

To Current Cost Reserve A/c. 4,500

(Monetary Working Capital Adjustment)

110 becomes the average price index.

Gearing Adjustment:

The current cost operating profit (CCOP) determined after making the above three adjustments is the true amount of profit from operations (ordinary activities of an enterprise) which can help the enterprise to continue to maintain its operating capability. However, the net operating assets which are used to indicate operating capability of a firm are likely to be financed partly by borrowings.

Therefore, the effect of the borrowings is considered while determining profit which can be distributed to shareholders. This effect is measured through calculating gearing ratio and subsequently the amount of gearing adjustment. No gearing adjustment arises, where a company is wholly financed by shareholder’s capital.

A company that has a large proportion of fixed interest and fixed dividend bearing capital to ordinary capital is said to be highly geared. While repayment obligations in respect of borrowings are normally fixed in monetary amount, the proportion of net operating assets so financed by borrowings increases or decreases in value to the business.

Thus, when these assets have been realised either by sale or use in the business, repayment of borrowing could be made so long as the proceeds are not less than the historical costs of those assets. It is, therefore, suggested that the current cost profit attributable to shareholders should be determined by taking into account the method of financing the net operating assets.

The current cost profit attributable to shareholders reflects surplus for the period after making allowance for the impact of price changes on funds needed to maintain the shareholder’s proportions of the net operating assets.

Thus, gearing adjustment is made where a proportion of the assets of business is financed by borrowing. Net borrowing is defined as the amount by which liabilities exceed assets. Liabilities and assets for the purpose of gearing adjustment are defined as follows:

Liabilities are the aggregate of all liabilities and provisions (including convertible debentures and deferred tax but excluding dividends) other than those included within monetary working capital. Assets are the aggregate of all current assets other than those that are subject to a cost of sales adjustment and those that are included within monetary working capital.

The gearing adjustment itself results from the application of the gearing ratio to the net adjustment made in converting the historical cost income to current cost income. The gearing ratio is found in the relationship between net borrowings and average net operating assets. Average net operating assets is obtained from the opening and closing net operating assets divided by two.

The gearing ratio formula is:

![]()

Net borrowings = All liabilities and provisions including convertible debentures and deferred tax but excluding dividends and items included in MWCA

minus

All current assets other than items included in MWCA and COSA.

If the total of current assets (bank balance) is more than the current liabilities, no gearing adjustment is calculated.

Sometimes, gearing ratio is calculated using average equity capital, as follows:

![]()

Current Cost Reserve:

Current cost accounting suggests the creation of a reserve account, known as current cost reserve account.

The current cost reserve includes:

(i) Current cost adjustments, i.e., depreciation backlog adjustment, cost of sales adjustment and monetary working capital adjustment,

(ii) Gearing adjustment,

(iii) Un-realised revaluations surpluses on fixed assets, closing stock and investment.

The gearing adjustment amount is credited to profit and loss account and debited to Current Cost Reserve Account.

Example:

Assume a company has a capital mix of 40 per cent debt and 60 per cent equity. The following amounts of adjustments have been found using CCA method:

In the above case debt constitutes 40 per cent of the total capital. Therefore, the amount of gearing adjustment will be Rs. 22,000 (Rs. 55,000 x 40%). It means only Rs. 33,000 which represents shareholders’ share will be charged to Profit and Loss account. The Current Cost Reserve Account will be credited with the amount of Rs. 33,000 on account of three adjustments.

Alternatively, more preferably, Rs. 55,000 is charged to Profit and Loss account. Since the amount of gearing adjustment is credited to Profit and Loss account, the net effect is that only Rs. 33,000 stands charged to Profit and Loss account. Also, gearing adjustment is debited to Current Cost Reserve account.

(B) Preparation of Current Cost Balance Sheet:

Under current cost accounting, current cost balance sheet is prepared.

Balance sheet items are treated in the following manner:

(1) Fixed Assets:

The fixed assets should be shown in the balance sheet at their value to the business. The value of the business of an asset is the amount which the business would lose if it were deprived of that asset.

Determining the value to the business, i.e., generally the current cost of fixed assets, involves great difficulty, because usually the assets now in use were acquired long ago than is typically the case with inventory, and the assets in use, if replaced currently, would be replaced by different assets.

Thus, if a used asset of like age and condition to the asset in use can be priced, that will set the current cost. If a new asset has to be used as the basis for pricing the old asset, adjustments have to be made for the differences in life expectancy, productive capacity, quality of service, and operating costs between the new and the old asset.

The concepts of gross and net current replacement cost are important in this context. The gross current replacement cost of an existing asset is the cost that would have to be incurred at the date of the valuation to obtain and install a substantial identical asset in new conditions. For example if a plant purchased on January 1, 2007 for Rs. 80,000 can be purchased on December 31, 2009, for Rs. 1,00,000, its gross current replacement cost on December 31, 2009, will be Rs. 1,00,000.

The net current replacement cost of an existing asset refers to that part of the gross current replacement cost which represents its unexpired service potential. For example, suppose the plant in the above example is estimated to have an economic life of five years. Since it has been used for three years, its net current replacement cost would be Rs. 40,000 (assuming that the equipment will have a zero scrap value at the end of its economic life).

In circumstances, where the asset in use would not be replaced, if for any reason it were taken out of service, its value to the business is not its current cost but a lower recoverable amount.

This recoverable amount is its value if sold or its value if used, whichever is higher. Its value if sold is its realisable value, net of selling costs. Its value in use is the net present value of future cash flows (including the ultimate proceeds of disposal) expected to be derived from the use of the asset by the enterprise.

(2) Land and Buildings:

The land and buildings occupied by the owner himself, should be shown in the balance sheet at their value to the business which will normally be the open market value for their existing uses, plus estimated acquisition costs.

However, in cases where an open market valuation of the land and buildings as a whole cannot be made, the net replacement cost of the buildings and the open market value of land for its existing use plus the estimated acquisition costs should be taken as their value to the business. The valuation should be made by professionally qualified valuers at periodic intervals.

(3) Inventories:

In the balance sheet, inventories should normally be shown at the lower of the current replacement cost as on the date of balance sheet and the net realisable value.

Revaluation Surplus Transferred to Current Cost Reserve Account:

Increase in the value of fixed assets like plant and machinery, land and building, closing stock, investment is credited to current cost reserve account The increase in value of fixed asset is arrived at by deducting the net historical cost of the asset from its net current cost at the end of the year, both sums being calculated before taking depreciation into account.

To take an example, assume a plant was purchased for Rs. 1,20,000 having a useful life of ten years. Its replacement cost now is Rs. 1,80,000.

In the fifth year, the amount to be transferred to current cost reserve account will be Rs. 36,000, calculated as follows:

The profit and loss account, balance sheet and current cost reserve account under current cost accounting will appear as follows:

Current Cost Accounting (CCA) Profit and Loss Account:

Notes:

1. Alternatively, gearing adjustment amount could be deducted from the total of current cost operating adjustments (dep. adjustment, COSA and MWCA). The result will be the same if gearing adjustment is deducted from current cost adjustments, or if not deducted from current cost operating adjustment and subsequently added to current cost profit.

2. Gearing adjustment is calculated only when a firm is financed partly by borrowing. No gearing adjustment arises when a company is wholly financed by shareholders’ capital. To find out the net borrowings, cash balance is deducted from total borrowings. Or if cash balance is more than the borrowings, there will be no gearing adjustment.

The above profit and loss account (prepared in a statement format) can be shown in a T format, as below:

Illustrative Problem 2:

A company buys and sells goods. During the three months ending March 31, 2009, the company enter into the following transactions:

Illustrative Problem 3:

The following are the profit and loss account for the year ending December 31, 2008 and balance sheets as at December 31, 2008 and December 31, 2009 prepared on historical cost basis:

The following additional information has been provided:

(i) The general purchasing power price-level indices for 2008 and 2009 were as follows:

(ii) Fixed assets were acquired when the purchasing power index was 100.

(iii) All transactions, sales and purchases occurred evenly throughout the year.

(iv) Stock at January 1, 2009 was acquired evenly during the last three months of 2008.

(v) Stock at December 31, 2009 was acquired evenly during the last three months of 2009.

(vi) Depreciation of plant and machinery is at the rate of 14% on cost.

(vii) The specific price indices relating to plant and machinery were as follows:

(viii) The specific price index was 100 when the plant and machinery was purchased.

(ix) The specific price indices for stock were as follows:

(x) The specific price indices used for stock are to be used in computing the monetary working capital adjustment.

(xi) The freehold premises were valued on an existing use basis, the value being Rs. 45,000 at December 31, 2008 and Rs. 75,000 at December 31, 2009.

(xii) The aggregate monetary working capital adjustment to December 31, 2008 was Rs. 2,130 and the aggregate cost of sales adjustment was Rs. 6,907. The accumulated depreciation adjustment to December 31, 2008 is to be charged equally between the profit and loss account and the current cost reserve.

(xiii) The debenture interest was paid on December 31, 2009.

Evaluation of Current Cost Accounting:

The adoption of current cost or lower recoverable amount in place of historical cost as the attribute to be used for measuring assets and if relevant, liabilities also, would greatly increase the relevance of information conveyed in financial reports, and it would increase its utility and representational faithfulness.

It is important that the value of an item to the business must be capable of being determined reliably; if this cannot be done, a surrogate for it must be found satisfactorily.

The basic objective of current cost accounts is to provide more useful information than that available from historical cost accounts for the guidance of management of the business, the shareholders and others on such matters as the financial viability of the business, return on investment; pricing policy, cost control and distribution decisions; and gearing.

The current cost accounting possesses the merit of closely approximating the impact of specific price changes on the business enterprise because it makes use of specific indices. The CCA measures an individual company’s experience of inflation by reference to that company’s specific pattern of expenditure.

As such, the method seeks to maintain the operating capability of the enterprise during inflation. The same tools of analysis as those applied to historical cost accounts are generally appropriate.

The ratios derived from current cost accounts for such items as gearing, asset cover, dividend cover and return on capital employed will often differ substantially from those revealed in historical cost accounts but should be more realistic indicators when assessing an entity or making comparisons between entities.

SSAP 16 points the limitations of CCA as follows:

“As with historical cost accounts, CCA (based on value to tile business concept) is not a substitute for forecasting when such matters as a change in the size or nature of the business are consideration. It assists cash flow forecasts, but does not replace them. It does not measure the effect of changes in the general value of money or translate the figures into currency of purchasing power at a specific date. Because of this it is not a system of accounting for general inflation. Further, it does not show changes in the value of the business as a whole or the market value of the equity.”

An important weakness of this model is that is seems to possess an element of subjectivity inherent in periodic revaluations, specially where specific price indices are not generated by an authoritative agency.

Furthermore, perhaps the largest problem is the aggregation problem. The value to the firm principle has its theoretic roots in the valuation of the individual assets, not the firm as a whole, but accounts, whether balance sheets or profit and loss accounts, are aimed at the assessment of the performance of the business as a whole.

Other important problems include the precise definition of replacement cost under conditions of economic and technological change: replacement cost is fundamental to the value to the firm method.