It may happen in case of new companies that a running business is taken over from a certain date, whereas the company may be incorporated at a later date. The company would be entitled to all profits earned after the date of purchase of business unless the agreement with the vendors provides otherwise.

But profits up to the date of incorporation of the company have to be treated as capital profits because these are the profits which have been earned even before the company came into existence. Such profits are known as profits prior to incorporation. It should be remembered that a public company cannot commence business till it receives the certificate of commencement of business.

Therefore, it would be prudent to treat all profits earned before commencement of business as capital profits. However, strictly speaking, “Profit Prior to Incorporation” means only the profits earned up to the date of incorporation and not up to the date of the certificate of commencement of business.

For correct allocation of profits, a profit and loss account should be prepared on the date of incorporation; but this would mean taking stock which is inconvenient. The usual practice, therefore, is to prepare the profit and loss account only at the end of the year and then to allocate the profit between the two periods—up to incorporation and after.

ADVERTISEMENTS:

The allocation is done on the following basis:—

(a) Gross profit should be allocated according to the ratio of sales for the two periods.

(b) Expenses that are connected with sales, (such as discount allowed, bad debts, commission to salesmen, advertising, etc.) should be allocated in the ratio of sales.

(c) Expenses that are incurred on the basis of time (such as salaries, rent, interest, etc.,) should be allocated in the ratio of the time before incorporation and after.

ADVERTISEMENTS:

(d) Expenses that are solely incurred for the company on and after its incorporation (for example, preliminary expenses or interest on debentures or directors’ fees) should be charged wholly to the post-incorporation period.

Gross profit minus the total of expenses for the pre-incorporation period will give the profit prior to incorporation.

The entry to be passed will be:

![]()

Profit Prior to Incorporation will appear in the balance sheet along with other capital profits. The remaining profits will be treated as revenue profits and available for dividends, etc.

ADVERTISEMENTS:

Illustration 1:

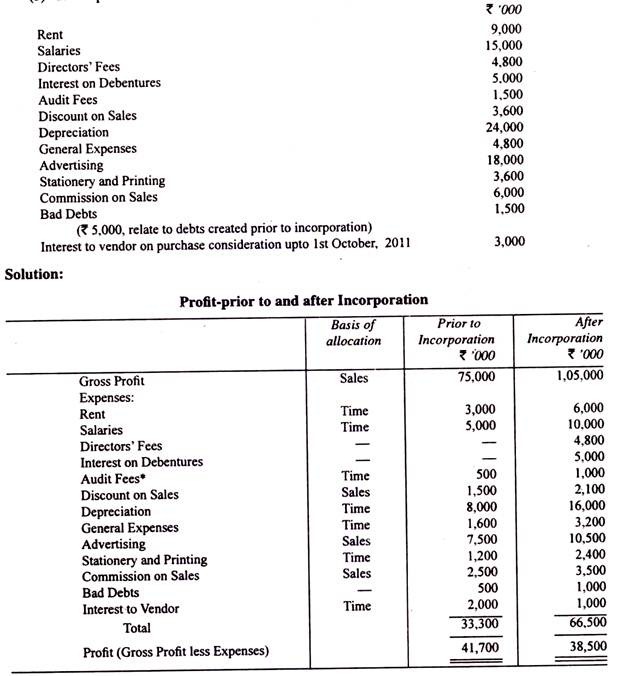

G Ltd. was incorporated on the 1st August, 2011 and received its certificate for commencement of business on 1st September, 2011. The company bought the business of M/s Active and Slow with effect from 1st April, 2011.

From the following figures relating to the year ending 31st March, 2012 find out the profits available for dividends:—

ADVERTISEMENTS:

(a) Sales for the year were Rs 60 crore out of which sales up to 1st August were Rs 25 crore and upto 1st September Rs 30 crore.

(b) Gross Profit for the year was Rs 18 crore.

(c) The expenses debited to the statement of Profit and Loss were:—

The ratio of sales is 25 crore: 35 crore or 5 : 7. The ratio of time is four months (up to 1st August) to 8 months or 1:2, except in case of interest to vendor. In this case (the interest paid is for 6 months out of which interest for four months (up to 1st August) is charged to the period prior to incorporation. Bad debts have been allocated according to the indication given in the question.

ADVERTISEMENTS:

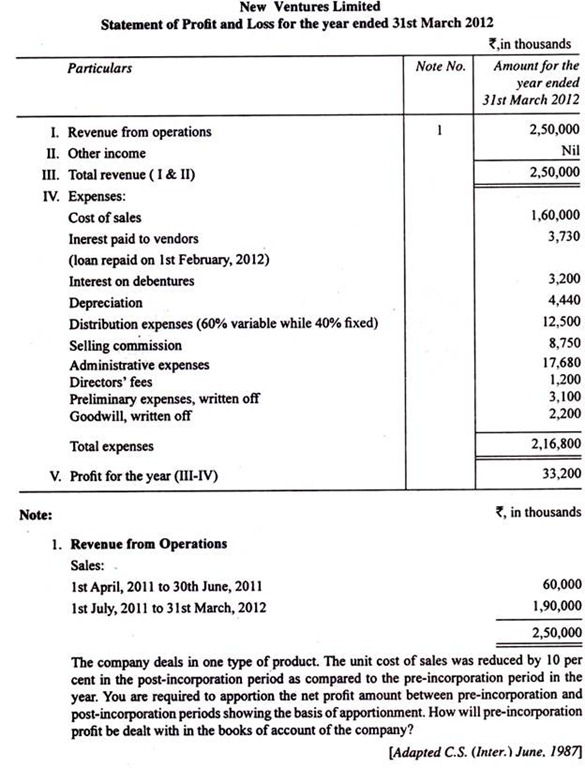

Illustration 2:

New Ventures Ltd. was incorporated on 1st July, 2011 with an authorised capital consisting of 50,000 equity shares of Rs 10 each to take over the running business of Random Brothers as from 1st April, 2011.

The following is the summarised Statement of Profit & Loss for the year ended 31st March, 2012:—

Sometimes, the sales figure for the period prior to incorporation is not given directly but has to be calculated from the ratio of sales of various months.

Suppose, (a) a company is incorporated on 1st August, 2011, having taken over a running business on 1st April, 2011; (b) sales for the year ending 31st March, 2012 are Rs 95 lakh; and (c) sales for the each one of the first five months of the accounting year are half of what they are for each one of the seven subsequent months of the accounting year.

Thus, if the sales figure for each one of the first five months is 1, the sales for each one of the subsequent seven months are 2; total for the first five months is 5 and that for the subsequent seven months 14. Now, sales for four months up to 1st August, 2011 would be 1 x 4 i.e., 4 and sales for the following eight months would be 1 + 2 x 7 or 1 + 14 i.e. 15.

ADVERTISEMENTS:

The ratio between pre-incorporation sales and post-incorporation sales is 4 : 15. Hence, total sales during the pre-incorporation period are Rs 95 lakh x 4/19 = Rs 20 lakh and the total sales during the post-incorporation period are Rs 75 lakh.

Examples:

(1) A company takes over a business w.e.f. 1st April, 2011 and is incorporated on 1st August, 2011, sales for the full year ending 31st March, 2012 are Rs 12 crore; the sales for the months of April, June and December are one and a half times the average; sales for the month of May are half the average and for march are twice the average.

The sales for the months of April to July will be calculated as under:

Illustration 3:

ADVERTISEMENTS:

A company was incorporated on 1st August, 2011 to take over a business from the preceding 1st April. The accounts were made upto 31st March, 2012 as usual and the statements of profit and loss gave the following result:

![]()

Illustration 4:

Green Company Ltd. was formed to take over a running business with effect from 1st April, 2011. The company was incorporated on 1st August, 2011, and the certificate of commencement of business was received on 1st October, 2011. The following profit and loss statement has been prepared for the year ended 31st March, 2012.