In this article we will discuss about the Current Cost Accounting (CCA):- 1. Introduction to Current Cost Accounting 2. Features 3. Evaluation 4. Conclusion 5. The Stand of the Institute of Chartered Accountants of India.

Contents:

- Introduction to Current Cost Accounting

- Features of Current Cost Accounting

- Evaluation of Current Cost Accounting

- Conclusion to Current Cost Accounting

- The Stand of the Institute of Chartered Accountants of India

1. Introduction to Current Cost Accounting:

The system of inflation accounting now accepted in U.K. is called the Current Cost Accounting System evolved in the initial stages by the Sandilands Committee. The system has been extensively studied and debated and now it has been finalised by the issue of SSAP 16 (Statement of Standard Accounting Practice).

ADVERTISEMENTS:

This system takes into account price changes relevant to the particular firm or industry rather than the economy as a whole. It seeks to arrive at a profit which can be safely distributed as dividend without impairing the operational capability of the firm. In addition to adjustments for depreciation and cost of sales, it deals with the working capital and also loans raised. The ambit is operation profit and operating capital employed.

Current cost accounting has the following important features:

(a) Fixed assets are to be shown in the balance sheet at their value to the business and not at their depreciated original cost.

(b) Stocks are to be shown in the balance sheet at their value to the business and not at the lower of their original cost and realisable value.

ADVERTISEMENTS:

(c) Depreciation for the year is to be calculated on the current value of the relevant fixed assets.

(d) The cost of stock consumed during the year is to be calculated on the value to the business of the stock at the date of consumption and not at the date of purchase.

(e) The effects of the loss or gain from loans will be computed and set off against interest.

The increased replacement cost of fixed assets and of stocks, the increased requirements for monetary working capital and the under provision of depreciation in the past years may be adjusted through a revaluation reserve.

ADVERTISEMENTS:

The fixed assets in the balance sheet should be shown at their ‘value to the business’, which is defined as the amount which the company would lose if it were deprived of the assets.

The value to the business can be defined in one of the following three ways.

(a) Net Replacement Value:

This refers to the money now required to buy a new asset of the same type as the existing one less an amount of depreciation that recognises the fact that the true replacement of the asset would not be a new asset but an asset which has the same remaining useful life as the existing asset.

ADVERTISEMENTS:

Suppose, a machine whose total life is 10 years can now be procured for Rs 80,000. Suppose further that the machine is 5 years old. Assuming that the machine has no scrap value, the net replacement cost of the machine would be Rs 80,000 minus depreciation for 5 years, i.e., Rs 40,000.

(b) Net Realisable Value:

This is the value which is represented by the net cash proceeds which would be received if the existing asset is sold now.

(c) Economic Value:

ADVERTISEMENTS:

This refers to the present value of the net income that will be earned from using the existing asset during the rest of its life. Suppose, the net cash inflow (gross income minus expenditure of the machine in our example) is Rs 8,000 per annum.

This means that in the 5 years of its remaining life it will yield 140,000 in all. Since the sum (Rs 40,000) will be accruing over the next 5 years and not immediately, it should be discounted and the present value of the future net cash inflows worked out.

The three values discussed above represent the purchase, sale and the holding value of the asset. According to the exposure draft, the net replacement cost is usually the best indicator of the value to the business of an asset.

The value to the business of the self-occupied land and buildings will normally be the open market value for their existing use plus estimated attributable acquisition costs. The depreciated replacement cost of the buildings and the open market value of land, including the estimated acquisition costs for the existing use, should be taken as their value to the business.

ADVERTISEMENTS:

Such as valuation should be made by a professionally qualified valuer at intervals of not more than 5 years. In the years between full scale professional valuations, the directors should estimate the value of the land and buildings after consultation with professional valuers and after taking into account market variations and changes in construction costs.

Plant and machinery should be valued at their net current replacement costs. For this purpose, the gross current replacement cost of plant and machinery should be worked out. This is the cost that would have to be incurred to obtain and install at the date of the valuation, a substantially identical replacement assets in new condition.

Since the plant and machinery is not new, the gross replacement cost arrived at as above should be written down with reference to the number of years that the existing plant and machinery has already served. In other words, depreciation should be charged on the gross current replacement cost on the basis of the expired service potential of the asset in question.

The gross current replacement cost can be known from the following sources;

ADVERTISEMENTS:

(i) The official price lists or the catalogues of the suppliers;

(ii) The estimates made by the company itself based on expert opinion;

(iii) Index compiled by the company from its own purchasing experience;

(iv) Authorised price indices prepared by external agencies like the Department of Industry or Central Statistical Organisation. These indices are now prepared in the U.K. both with reference to the category of assets and the type of industry.

Investments held by the company, not as current assets, should be valued at their value to business.

This implies that the quoted investments should be based on the stock market mid prices and the unquoted investments should be based on the directors’ valuation of, on the basis of the current cost, net asset value of the company in which the investments have been made or on the basis of the present value of the likely future income from the unquoted investments.

ADVERTISEMENTS:

In case investments are held as current assets, their treatment should be the same as that of stock and work in progress. In case of investments in subsidiaries, the cost of the shares should be adjusted to the movement in reserves or net assets of the subsidiaries after the shares have been acquired.

Stocks and work in progress should be shown in the balance sheet at their value to the business on the balance sheet date. The value to the business of a company’s stock is lower of the replacement cost of that stock and its net realisable value.

In other words, both the replacement cost of the stock and the net realisable value of the stock should be worked out. The lower of these two amounts would be the value which should be put to the stock in the balance sheet.

Debtors, cash and current liabilities in the current cost balance sheet are shown at their value to the business which is their net realisable value. It is obvious that these amounts would be the same in the historical cost balance sheet and the current cost balance sheet.

The depreciation charge in the current cost profit and loss account should be based on the current value of fixed assets. Thus, the depreciation charge may be based on the average of the opening current value and the closing current value.

Further, as the gross value of the asset increases in an inflationary period due to it being at its replacement cost, the accumulated depreciation will not be sufficient. Hence, additional depreciation should be charged to provide for this backlog.

However, this additional depreciation should be set off against the surplus arising on the revaluation of the assets. Suppose, a machine is purchased for Rs 10 lakh on 1st April, 2007. Suppose further that on 1st April, 2011, the current value of the machine is Rs 20 lakh and on 31st March, 2012, the current value of the machine is Rs 22 lakh.

The depreciation for the year ended 31st March, 2012 will be charged on Rs 21 lakh. If the life of the machine is 10 years, the depreciation for the year 2011 -2012 would be Rs 2,10,000. Suppose, the accumulated depreciation is Rs 7 lakh.

The total accumulated depreciation now becomes Rs 9,10,000. This is not enough at the gross replacement cost of the asset on 31st March, 2012. Depreciation on Rs 22 lakh for five years at 10%, straight-line basis, would be Rs 11 lakh.

Hence, a further depreciation charge of Rs 1,90,000 should be made. The depreciation of Rs 2,10,000 will be debited to the profit and loss account and the depreciation of Rs 1,90,000 will be set off against the revaluation surplus.

The figure for sales remains the same in the historical cost account and the current cost accounts. However, the cost of sales is different in the historical cost accounts and the current cost accounts. This is because in historical cost accounts each item of stock sold or consumed is included at FIFO cost.

The objective of current cost accounts is to charge against sales revenue, the value to the business of the costs consumed at the date they are consumed.

The date of consumption of stock is normally the date of sale and to arrive at the current cost of sale it is necessary to substitute the current replacement cost of stock sold at the date of sale in place of the historical cost of stock sold.

Since it may not be possible to know the current cost of sale of each individual item of stock, it is suggested that an overall cost of sales adjustment may be made. This adjustment is based on approximation through the averaging method.

It would thus be seen that the current profit and loss account requires two adjustments from the historical profit and loss account—firstly, additional depreciation and, secondly, cost of sales adjustment (including working capital adjustment). The total adjustments are again adjusted for loans taken.

2. Features of Current Cost Accounting:

Below we discuss briefly and illustrate main features of CCA and see to what extent it will achieve the objectives set out above.

The system concerns operating profits and, naturally, operating capital employed and seeks to make a clear distinction between profits that emerge according to present day terms through operations and profits and those that arise only because of increase in prices, i.e., holding gains.

This distinction is of vital importance for judging the efficiency of a firm —the profit and loss account on historical cost basis mixes up the two profits and, hence, makes judgment about operational efficiency very difficult.

The following are the main features of CCA:

(i) Ascertaining the present day values of fixed assets on the basis of either specific price indices for various fixed assets (different types of production equipment being treated as different assets), or if indices are not available, replacement cost or recoverable value whichever is lower.

Suppose an asset is acquired on 1st April, 2008 at a cost of Rs 10 lakh with an expected life of 10 years ignoring the scrap value. By 1st April, 2011 the price index for the asset rose by 60% and by 75% by the end of March, 2012.

The asset will be valued on historical cost (HC) basis and on CCA basis as shown below:

The CCA balance sheet will show the asset on 31st March, 2012 at Rs 10,50,000. The increase of Rs 4,50,000, from Rs 6,00,000 (HC basis) to Rs 10,50,000 (CCA basis), will be credited to a (capital) reserve styled as “Current Cost Accounting Reserve”. A similar treatment will be accorded to the increase in value of inventories — see (iii) below:

(ii) Charging the correct or real depreciation to the profit and loss account, hi the HC accounts, the depreciation, actually charged must have been Rs 1,00,000.

The proper depreciation, however, is Rs 1,67,500, i.e.,

(iii) Arriving at the current cost of materials consumed (at the time of consumption) and other costs incurred that enter into the computation of cost of sales, i.e., making a Cost of Sales Adjustment (COSA). Taking a very simple example, suppose on 1st April 2011, a firm had 1,000 tonnes of materials which it had acquired at a cost of Rs 30 per tonne and that in 2011 – 2012 it consumed 800 tonnes, making no purchases.

The price on April I, 2011 was Rs 35, the average price during 2011-2012 was Rs 40 and that on March 31, 2012, it was Rs 45. On historical cost basis, the amount debited to the profit and loss account would be Rs 24,000, i.e., 800 tonnes @ Rs 30.

On CCA basis, the amount charged would be Rs 32,000, i.e.. @ 40 per tonne. The HC balance sheet on 31st March, 2012 will show the stock at Rs 6,000, i.e. 200 tonnes @ Rs 30; the CCA balance sheet will record the value @ Rs 9,000 i.e., Rs 45 per tonne — the increase of Rs 3,000 over the HC basis will be credited to the Current Cost Accounting Reserve.

Information about quantities and the purchase price was also the price prevailing at the time of consumption may not be readily available, at least as far as outsiders are concerned. In such assets, adjustment may be made on the basis of relevant price indices.

Suppose the following HC information is available for a year:

On HC basis, the cost of materials consumed would be Rs 7,59,000 but on CCA basis it will work out to be Rs 8,58,000, as shown below on the assumptions that the consumption takes place regularly, say a month after the purchase, and that the rise in prices is uniform throughout the year

For the purpose of the CCA balance sheet, the closing stock would be written up to Rs 1,44,000, i.e., Rs 1,41,000 X 240/235, Rs 3,000 would be added to the Current Cost Accounting Reserve and Rs 99,000 i.e., Rs 8,58,000 less Rs 7,59,000 would be the Cost of Sales Adjustment.

Cost of Sales Adjustment would be necessary also for other items entering the computation of cost of sales, chiefly wages and other operating costs excluding depreciation. Suppose wages and other operating costs amount to Rs 20,00,000 in a year and it is estimated that the increase, Rs 1,00,000 should be the COSA in this regard.

(iv) Ascertaining the additional requirement of monetary working capital purely because of movement in prices and making an adjustment therefore (MWCA, or Monetary Working Capital Adjustment). It should be noted that the additional requirement due to a change in the scale of operations is to be ignored—only the effect of price changes is to be considered.

Monetary working capital normally, means the aggregate of: trade debtors, pre-payments and trade bills receivable less trade creditors, accruals and trade bills payable. The Adjustment required in regard to the monetary working capital will be based on the prices of materials in the case of trade creditors and of finished goods in the case of trade debtors.

Consider the following:—

Price in 2011-2012 for materials rose from 200 to 230 and for finished goods from 150 to 180. To ascertain the effect of price changes, first the volume increase should be established; for this purpose both the opening and closing balances should be adjusted on the basis of average movement of prices. Thus:

The increase in the monetary working capital because of volume changes is Rs.56, 250, whereas the actual increase is Rs.86, 000. Hence the difference, Rs.29, 750, is the required monetary working capital adjustment.

(v) Gearing Adjustment:

CCA is concerned with ascertaining profits as far as shareholders are concerned. It recognises that a part of the operating capital is obtained by way of loans or other monetary obligations which remain unaffected by changes in prices.

Therefore, a part of the adjustments in respect of depreciation for the current year, cost of sales and monetary working capital is ascribable to the loan funds or borrowings. In other words, the net total adjustment in respect of the three items mentioned above is to be reduced by the proportion that borrowings bear to (loosely speaking) the total operating capital employed.

In the examples given above, the various adjustments are the following:—

These amounts would be charged to the profit and loss account and credited to the Current Cost Accounting Reserve.

It borrowings are 40% of the funds employed (discussed below),Rs.1,18,500 would be credited to the profit and loss account by debit to the Current Cost Accounting Reserve.In the profit and loss account, the net of the gearing adjustment and the interest to be paid may.be shown.

SSAP 16 defines net borrowing as the excess of:

(a) The aggregate of all liabilities and provisions fixed on monetary terms (including convertible debentures and deferred tax but excluding proposed dividends) other than those included with monetary working capital and other than those which are, in substance, equity capital over.

(b) The aggregate of all current assets other than those subject to a cost of sale adjustment and those included within monetary working capital.”

Examples of (a) would be debentures, loans, provision for tax, etc., and of (b) cash and bank balances and marketable securities.

The equity funds would be all funds belonging to the shareholders on the basis of current cost accounting. The total operating capital would comprise net borrowings and equity funds. If B represents net borrowing and S equity funds, the gearing adjustment would be made on the basis of the ratio B/B+S For greater accuracy, the average of the ratio in the beginning and at the end should be used.

Illustration 1:

Below is given a simplified balance sheet and statement of profit and loss of a company in existence for about 10 years:

*Depreciation charge really comes to Rs 124 lakh.

The following facts are established:

(1) The price indices of tangible assets had climbed to 200 in the beginning of 2011-2012 and to 225 by the end of the year with the prices ten years ago being 100; the price increase in 2010-2011 was only 6%. Till the end of2010-2011 the company had not made any substantial additions to the tangible assets. The company considers the life of the tangible assets to be 20 years and would prefer the straight line basis of depreciation.

(2) Prices of materials rose by 54% and of finished goods by 35% during 2011-2012; rates relating to manufacturing costs increased by 20%.

(3) The value of finished goods stock in the beginning and at the end of the year was respectively Rs 158 lakhs and Rs 203 lakhs.

Prepare the current cost accounting balance sheet as at 31st March, 2012 and statement of profit and loss for the year 2011-2012 on that basis.

Solution:

The following assumptions are made:

(a) Material stocks are valued on FIFO basis.

Some Observations:

The accounts given above are naturally much too simple compared to the actual situation but, nevertheless, they are based on reality.

The following observations on these accounts may be pertinent:—

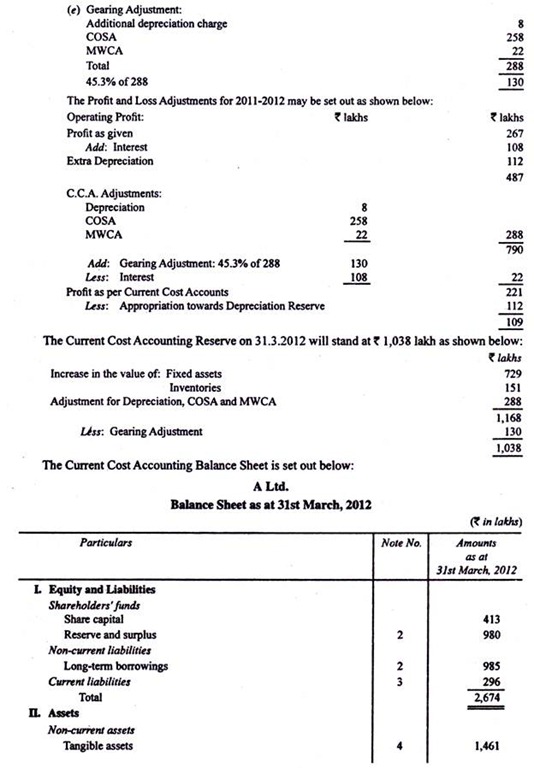

(i) The additional depreciation for the current year is only Rs 8 lakh; this low figure is because the depreciation actually charged in the accounts is much higher than that warranted on straight line basis with a life of 20 years. Generally, in industrial concerns the adjustment required for depreciation will be heavy.

(ii) COSA in the above case is very large. This is because there was a very big increase in the prices of materials — 54%. Normally, the adjustment may not be large. Still the point that emerges is that if prices rise rapidly and if there is big time lag between purchase and consumption, the adjustment in respect of cost of sales will be material. Trading concerns cannot naturally ignore COSA.

(iii) The gearing adjustment has reduced the debit to the Profit and Loss Account by Rs 130 lakhs. Indian companies normally resort to loans in a big way and, hence, for Indian companies this adjustment will be generally substantial. In the case under discussion, interest payment was only Rs 108 lakhs, showing that due to rise in prices, there was a saving of Rs 22 lakhs because of the fixed nature of monetary obligations.

Illustration 2:

On 31st March, 2002, when the general price index was say 100, Forward Ltd. purchased fixed assets of Rs one crore. It had also permanent working capital of Rs 40 lakh. The entire amount required for purchase and permanent working capital was financed by 10% redeemable preference share capital. Forward Ltd. wants to maintain its physical capital.

On 31st March, 2012, the company had reserves of Rs 1.75 crore. The general price index on this day was 200. The written down value of fixed assets was Rs 10 lakh and they were sold for Rs 1.5 crore. The proceeds were utilised for redemption of preference shares.

On the same day (31st March, 2012) the company purchased a new factory for Rs 10 crore. The ratio of permanent working capital to cost of assets is to be maintained at 0.4 : 1.

The company raised the additional funds required by issue of equity shares.

Based on the above information (a) Quantify the amount of equity capital raised and (b) Show the Balance Sheet as on 1.4.2012. [Adapted C.A. (Final) May, 1998]

Illustration 3:

Zero Limited commenced its business on 1st April, 2011, 2,00,000 equity shares of Rs 10 each at par and 12.5% debentures of the aggregate value of Rs 2,00,000 were issued and fully taken up.

The proceeds were utilised as under:

Illustration 4:

The following date relate to Bearing Ltd:

3. Evaluation of Current Cost Accounting:

One may say that as for as measurement of real profits is concerned, CCA does an admirable job; it also partially fulfills the function of compelling the firm to accumulate funds, by way of depreciation, at a level much higher than under the HC system.

The following points of criticism against the CCA can still, however, be made:

(a) The system ignores, in reality, the question of backlog depreciation; even if from the very beginning inflation is kept in view, the accumulated depreciation will not be equal to the funds ultimately required for replacement.

Properly, the back long depreciation should be charged against revenue reserves available for dividend — only then will management be restrained from disposing of profits required really for replacement of funds.

This question can be solved in quite a few ways, one of which is to credit the Depreciation Provision annually by the interest saved by the firm by employing the funds internally. These is no doubt that attention needs to be paid on a systematic basis to ensure proper replacement.

(b) Even if the depreciation funds are adequate for replacement, they will be adequate for replacement of similar assets; they may not suffice for moving into another industry. It is surely the duty of management to do constant and serious thinking about its business policies and take stock of its resources, including financial resources, and husband them properly.

(c) COSA will be an important figure generally. However, cannot the work be simplified by adopting the base stock method? If this system is adopted and the stocks in excess of base stocks are valued on LEFO basis, cost of sales in respect of materials consumed will be generally the real cost of sales — the difference, if any, will be so small as well make no difference.

(d) Similarly, for the sake of simplicity, the monetary working capital adjustment may be arrived at by applying the percentage increase in price of materials to the creditors in the beginning and the increase in price of finished goods to sundry debtors in the beginning and establishing the difference between the two figures thus arrived at.

It is not a fine calculation but it will give quite accurate figures of additional monetary working capital required as a result of movement in prices, ignoring volume changes during the year.

(e) The system recommends gearing adjustment to be made in respect of current year’s depreciation, COSA and MWCA. The reason why it should not apply to revaluation profits is not at all clear. The rationale behind the gearing adjustment is that part of the operating funds is raised by way of borrowings, fixed in monetary terms.

This holds goods for all operations and, if gearing adjustment is in order, it should be in order for all profits (or losses) resulting from taking into account price level changes. Further the application of gearing adjustment seeks to imply that the objective of accounting is to ascertain the profit for shareholders and not the firm.

This appears to be wrong — the objective should be to ascertain profit of the firm and not for any of the interested parties. The management can certainly arrive at the profits that can be properly distributed among the shareholders even on the basis of the profit for the firm.

There is one point in favour of gearing adjustment. It shows clearly the real annual cost of borrowing since interest paid is adjusted against the gearing adjustment. The gains made by the firm by borrowing in inflationary times are brought out by the adjustment. Still on the whole, gearing adjustment does not appear to be theoretically sound.

4. Conclusion to Current Cost Accounting:

Materiality is a recognised principle in accounting; in this regard inflation accounting is not an exception. The implication is that each firm should decide for itself whether any of the adjustments required under CCA can be ignored. Suppose a firm, like an oxygen company, does not use much material; it can probably ignore COSA. Each industry should consider and decide on the extent of applicability of the various adjustments.

Though survival is the prime concern of the management and this should not depend on other considerations, like the attitude of tax authorities, yet many firms will not agree to inflation accounting unless Government and revenue authorities agree to allow depreciation on the basis of present day values.

For this purpose, a consensus between industry, the accounting profession and the Government will be essential.- The Government has itself a vital interest since it is obviously concerned with prevention of sickness. It is time, therefore, that like the Government in U.K., the Government of India also takes the initiative.

One cannot say that all the recommendations contained in SSAP 16 should apply to India — the system will require implication before application in this country. But it must ensure proper financial measures to the extent accounting can do that to see that replacement of assets when due is carried out without difficulty.

It is expected that the Institute of Chartered Accountants of India will soon make known its recommendations about inflation accounting.

5. The Stand of the Institute of Chartered Accountants of India:

The Institute recommends the adoption of inflation accounting but recognises that much care and caution will have to be taken. It favours the adoption of the Current Cost Accounting Method but would permit not only the CPP Method but also even revaluation of fixed assets and adoption of the LIFO basis as regards inventories. In its “Guidance Note on Accounting for Changing Prices” (published in December 1982), the Institute makes the following recommendations;—

37. The adoption of a system of accounting for changing prices would require a considerable amount of time, money and specialized skills. Also the various techniques are still in the process of development. However, in view of the importance of the subject, it is recommended that enterprises, particularly the large enterprises, may develop the necessary systems to prepare and present this information.

38. Out of the various methods of accounting for changing prices discussed above, the Current Cost Accounting method seems to be most appropriate in the context of the economic environment in India. The periodic revaluations of fixed assets and the adoption of LEFO formula for inventory valuation are partial responses to the problem of accounting for changing prices. Current Purchasing

Power Accounting, though simple to apply, does not ensure the maintenance of the operating capability of an enterprise. Current Cost Accounting, on the other hand, is a rational and comprehensive system of accounting for changing prices, as it considers the specific effects of changing prices on individual enterprises and thus ensures that profits are reported only after maintaining the operating capability.

However, the introduction of a full-fledged system of Current Cost Accounting on a wide scale in India will inevitably take some time. During this transitional phase, periodic revaluations of fixed assets along with adoption of LIFO formula for inventory valuation would reflect the impact of changing prices substantially in the case of manufacturing and trading enterprises.

39. Adequate data base has presently not been developed in India for accounting for changing prices. Therefore, every enterprise may have to select the price indices depending on its own circumstances. The detailed price published in its monthly bulletin by the Government of India can be adopted in a number of cases.

There is no doubt that further steps will have to be taken for the timely publication of statistical information required by various industries for the implementation of accounting for changing prices.

40. Considering the importance of the information regarding the impact of changing prices it is recommended that while the primary financial statements should continue to be prepared and presented on the historical cost basis, supplementary information reflecting the effects of changing prices may also be provided in the financial statements on a voluntary basis, at least by large enterprises.

41. Since the presentation of statements adjusted for the impact of changing prices is voluntary, the enterprises may or may not get this information audited. However, the audit of such statements would enhance their credibility.

42. Apart from its utility in external reporting, accounting for changing prices may also provide useful information for internal management purposes. Accounting information system is designed primarily to provide relevant information to various levels of management with a view to assist in managerial decision-making, control and evaluation.

However, in periods of rapid and violent fluctuations in prices, the information provided by historical cost-based accounting system may need to be supplemented by information regarding the impact of changing prices.

The areas in which such information may be of prime importance to management include investment decisions and allocation of resources, divisional and overall corporate performance evaluation, pricing policy, dividend policy, etc.

43. In countries like the United Kingdom, there have been some reforms in the tax structure in the wake of introduction of accounting for changing prices. Though, the tax legislation in India at present does not give recognition to such an accounting system, even then accounting for changing prices would be useful for generating relevant information for internal and external decision-making….”.