Here is a compilation of top three accounting problems on underwriting of profit with its relevant solutions.

Problem 1:

A company incorporated on 1st April to acquire the running business of partnership firm from 1st January. Accounting year ends on 31st December.

Find out the Sales Ratio of pre- incorporation and post-incorporation periods from the following information:

ADVERTISEMENTS:

1. Sales for the whole year (Jan. to Dec.) Rs. 7, 20,000

2. Sales for January, June and July twice the average.

3. Sales for August VA times of the average.

4. Sales for March and September ‘A of the average.

ADVERTISEMENTS:

Solution:

Problem 2:

ADVERTISEMENTS:

New Ventures Limited was incorporated on 1st January with an authorised capital consisting of 5,000 Equity Shares of Rs. 10 each to take over the running business of Rundown Brothers as from 1st October 2003.

The following is the summarised Profit and Loss Account for the year ended 30th September 2004:

The company deals in one type of product. The unit cost of sales was reduced by 10% in post-incorporation period as compared to the pre-incorporation period in the year.

ADVERTISEMENTS:

You are required to prepare a statement apportioning the net profit amount between pre- incorporation and post-incorporation periods showing the basis of apportionments.

Solution:

Unit cost of sales was reduced by 10% in post-incorporation period. Therefore, if cost of sales is 100 in the pre-incorporation period, it would be 90 in post-incorporation period. Thus the ratio of cost of sales in pre- and post-incorporation period is 100: 90 or 10: 9. The sales figure was 6,000 and 19,000, therefore, the ratio is: (10 x 6,000): (9 x 19,000) (or) 60: 171 @ Interest to vendors:

ADVERTISEMENTS:

Pre-incorporation period is 3 months (Oct. to Dec.) Post-incorporation period is 1 month (Jan.). Thus ratio is 3: 1

Note:

The pre-incorporation profit may be used in writing off the Goodwill and Preliminary Expenses. Then the portion not covered by it, may be written off against post-incorporation period.

Alternatively, the Goodwill and Preliminary Expenses can be debited to after incorporation period.

ADVERTISEMENTS:

Problem 3:

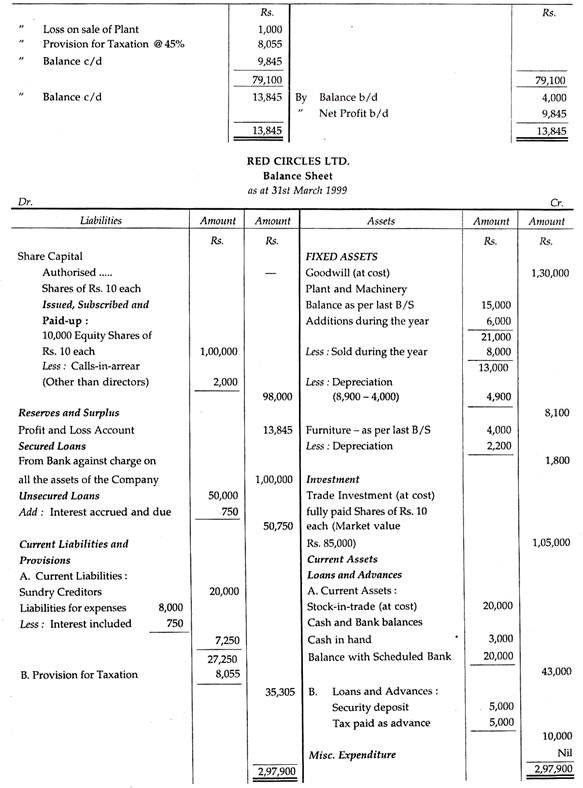

Singh Brothers Private Limited was incorporated on 1 st July 2003 with an authorised capital of Rs. 5, 00,000 in Equity shares of Rs. 10 each to take over a going concern as from 1st April 2003 should belong to the Company. The purchase consideration of Rs. 2, 00,000 together with interest @ 8.75% p.a. was satisfied on 1st October 2003 by the allotment to the Vendors 17,500 Equity shares fully paid and the balance in cash.

ADVERTISEMENTS:

The Trial Balance of the Company on 31st March 2004 was as follows:

You are required to prepare the Profit and Loss Account of the Company for the year ended 31st March 2004 and a Balance Sheet as on that date after taking into account the following:

1. Stock on 31st March 2004 Rs. 1, 40,000

ADVERTISEMENTS:

2. Bad Debts Rs. 500 (including Rs. 200 out of the book debts taken over by the vendors) to be written off.

3. Provision for Doubtful Debts to be made at Rs. 2,500.

4. Depreciate Buildings by 5% and Furniture by 10%.